Just A Spark

Open Interest is showing us that a little spark could lead to something much larger. And here's how to position yourself.

Noise was everywhere.

The sound of steam from the coffee maker.

The overtly creepy old man hitting on the young female barista.

The couple a few stools over making plans for their trip to Europe.

But I heard nothing…

One moment I was distracted by sensory overload, the next I was in my own world.

Never doubt what a strong cup of coffee can do to your focus.

Next thing I knew, the US market was closed, and my work day done. I flipped through my charts one last time, added a few notes, and got up to leave.

As I did, I paused before opening the door. Above me hung an all too familiar quote from a Bukowski poem:

It needn’t be much, just a spark.

A spark can set a whole forest on fire.

Just a spark.

I smirked. How fitting that is today.

The reason being, Bitcoin’s market structure at present looks like a powder keg in search of such a spark to ignite volatile price action.

Let me show you what’s brewing beneath the surface of the recent $70,000 reclaim.

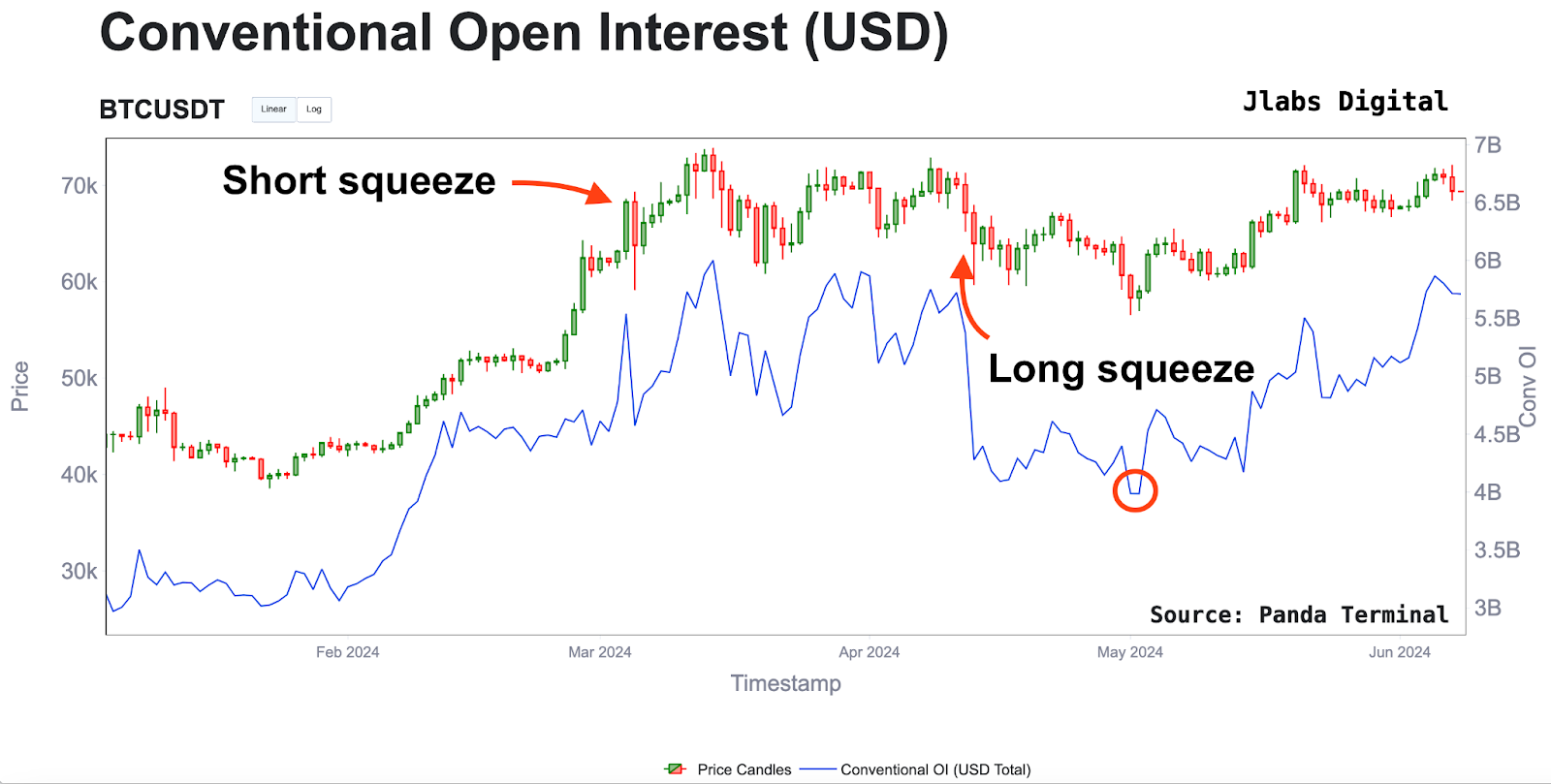

The Powder Keg

Below is a picture of the Bitcoin market’s powder keg.

It’s the amount of open interest in the perpetual markets as measured in USD. As we see, it’s gone absolutely parabolic since May 1st, which was when it bottomed out around $3.98 billion, having since moved up by 50% to surpass the March highs over $6 billion.

The reason this is a powder keg is because these positions can be liquidated with force. What I mean by that is if price reaches certain levels, the owners of these contracts can be forced to automatically buy back their positions if short, or sell if long.

This setup for these conditions is high open interest. It often precedes major moves in both directions and acts like an accelerant on price when perpetual players are squeezed out of the market during a trend change.

We can look back just over the last few months to see two examples of these washouts. And in both examples, high volatility followed:

- Late February when BTC broke past $60,000 in a parabolic fashion and wiped out billions of short OI en route to new ATHs.

- Mid-April when BTC dropped from $70,000 to $60,000 over the weekend and liquidated billions of dollars worth of longs.

This excessive positioning in the perpetuals market over the past month is very interesting. That’s because of three things. We have the always volatile CPI and FOMC events scheduled on deck for next week, BTC’s most recent move above $70,000, and an options market that seems indifferent to all of the above.

To better understand that last part, let’s take a closer look at the options data.

Diverging Options

This week, the most notable aspect of the Bitcoin options market has been the underwhelming performance of volatility. We can see that by glancing at the BVIV index in orange below.

As we see here, volatility as measured by the orange line is near multi-month lows at 50. This is despite Bitcoin recapturing the key psychological level of $70k and the abundance of OI mentioned above.

It’s a contradiction of sorts.

If we look back to March of this year when price was crossing $70k, IV was skyrocketing alongside price.

In that timeframe traders were piling into short-dated call positions, hoping to front-run a surge to new all-time highs. This caused implied volatility levels to run hot.

This time, is different. The market seems to have learned its lesson about FOMOing into calls and is largely skeptical of this rally's ability to push towards new ATHs. This sentiment for calls would likely change rapidly if Bitcoin were to experience a spot driven rally above $72,000, but not sooner.

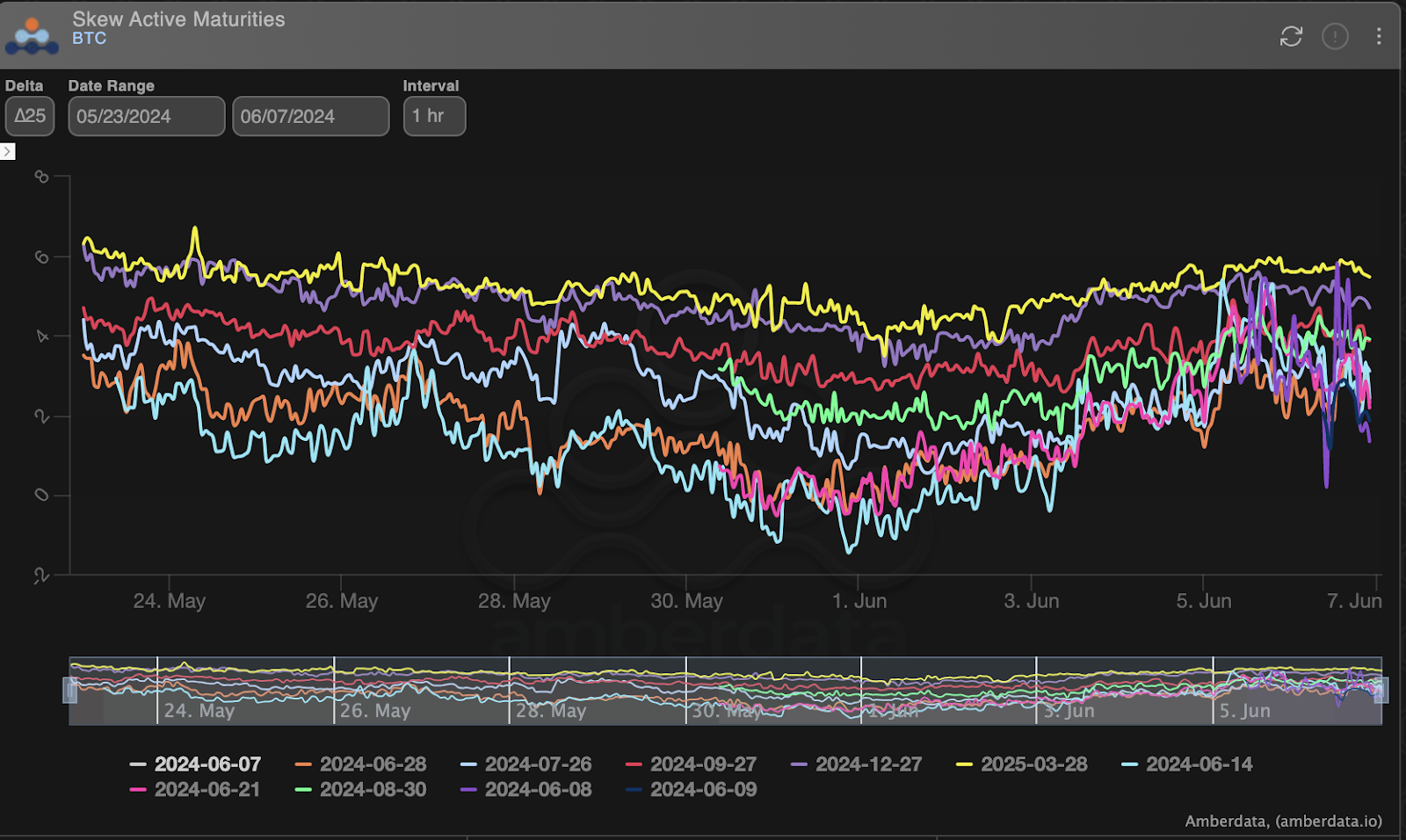

The market is also not that interested in buying put protection either.

As we can see in the chart below, the 25-delta put-skew, or the cost for downside protection vs the cost for upside exposure to price, remains firmly positive across all expiries. This tells us that the market is in no rush to hedge it’s downside exposure with options.

In any case, this is making short dated puts aka downside insurance cheaper than it has been in a while. An odd anomaly considering the macro events on deck for next week.

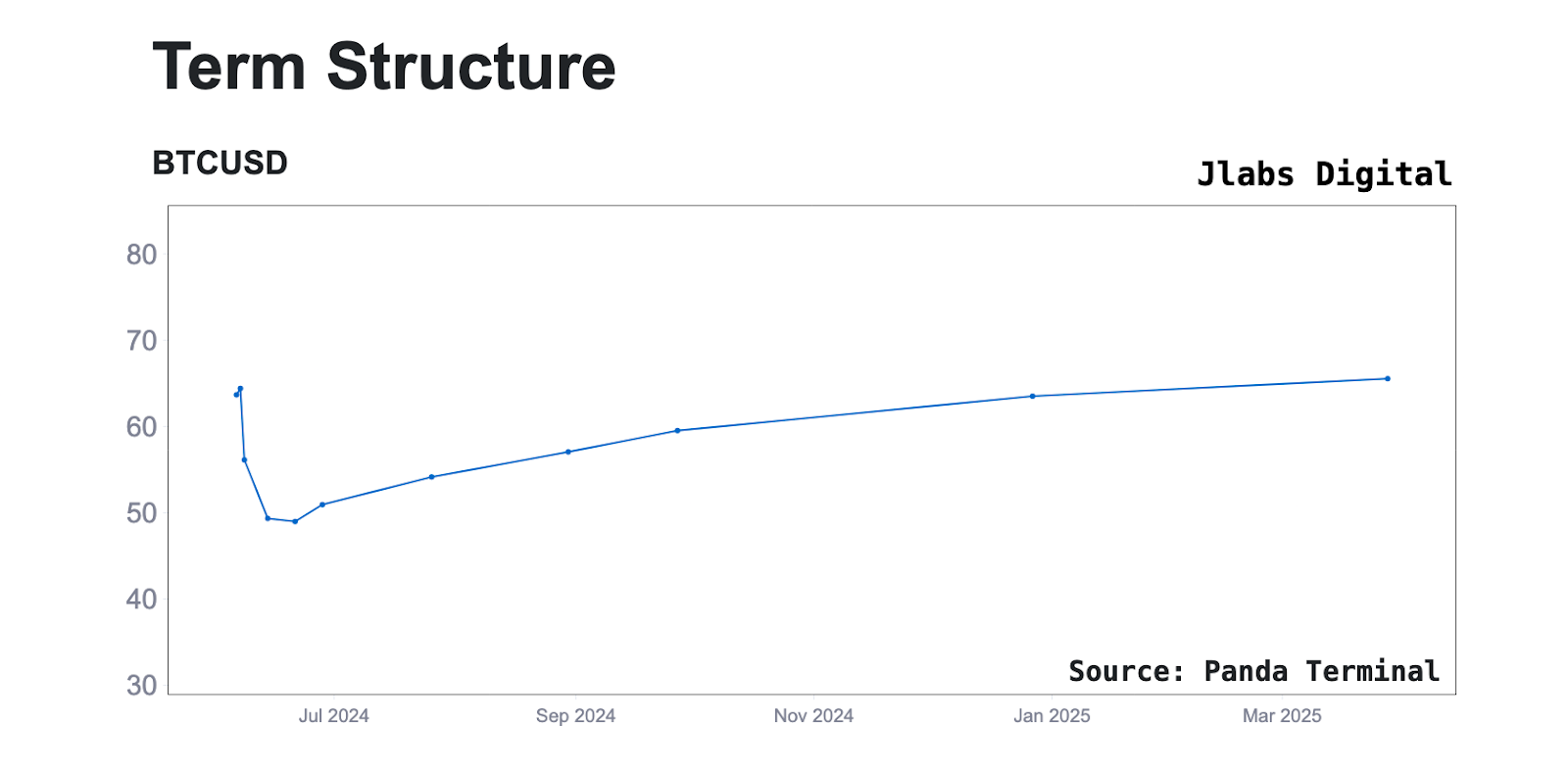

Observe The Curve

Due to this overall lack of demand in both directions the options market has turned into a one-way street.

Many are looking to sell options and harvest premiums, and very few are willing to take the other side of that as directional owners of volatility.

This is surprising.

In fact, we don’t see a single contract, even the furthest dated ones for March 2025, trading above 70. We can see this in the term structure chart below which plots the IV for contracts at the money for each expiry.

It’s a sign that the market is not pricing a move out of range in either direction anytime soon.

Everyone seems to have checked out for the summer.

Fortunately, like we discussed regarding Ethereum last week, these low volatility expectations offer their own set of opportunities….

For instance, the chance to gain volatility exposure in both directions.

We have a possible FOMC open interest wash-out next week or a parabolic ATH break over the summer. Whatever the scenario, position for either is cheap on a relative basis due to the lack of demand.

If on the other hand the perpetuals powder keg of OI unwinds, that’s ok as well. It’ll lead to more chop and long dog days of summer mentality.

Such a situation would make those Q4 contracts very attractive from a risk:reward perspective as Bitcoin will have then spent nearly 6 months consolidating between $60,000 - $70,000, and thus increasing the likelihood of a high velocity move out of range into the end of year.

IV levels would be in the bargain bin.

In either event, the powder keg is becoming more tightly packed with each day that Bitcoin remains range bound.

Now we just need a well timed catalyst to spark it and bring volatility burning back to life….

Until next week.

Watching the tape,

JJ