Crypto’s Ambulance Chasers May Be Headed for Trouble

Notes From the Lab: Are sellers of “paper” Bitcoin about to enter a world of pain?

A dark black box of unknown and incomprehensible risk.

That’s what you’re essentially placing your money into each time you make a deposit on most crypto exchanges.

You deposit your hard-earned cash, Bitcoin (BTC), or Ethereum (ETH), and in exchange, you receive 1 digital IOU on the company’s private ledger, allowing you to redeem your holdings at a future date.*

The asterisk here of course means that you have to trust in the exchange owners not to embezzle and/or gamble away your savings, as was the case with Celsius, BlockFi, and FTX.

It’s a system totally reliant upon trust rather than transparency, a trust in financial institutions which has been betrayed time and again not just in crypto, but throughout human history.

In the most recent case of FTX, for instance, when it claimed bankruptcy, its balance sheet showed it owed nearly 70,000 BTC to depositors.

This implies that as FTX circled the toilet bowl in its final days, SBF and company made the decision to sell all 70,000 of their customers’ Bitcoin (without consent) in a final act of desperation to save their sinking vessel.

It brings to mind one of the most popular sayings in crypto:

“Not your keys, not your coins.”

A lesson many crypto market participants have now learned in the harshest manner possible, just like the first generation of Bitcoin traders who were burned by the hack of Mt. Gox in 2014.

A baptism by fire, but sometimes, that’s the best way to learn.

Today, let’s take a look at how the second-order effects of FTX’s fallout are changing market structure, and potentially setting us up for the mother of all short squeezes…

Bank Run in Progress

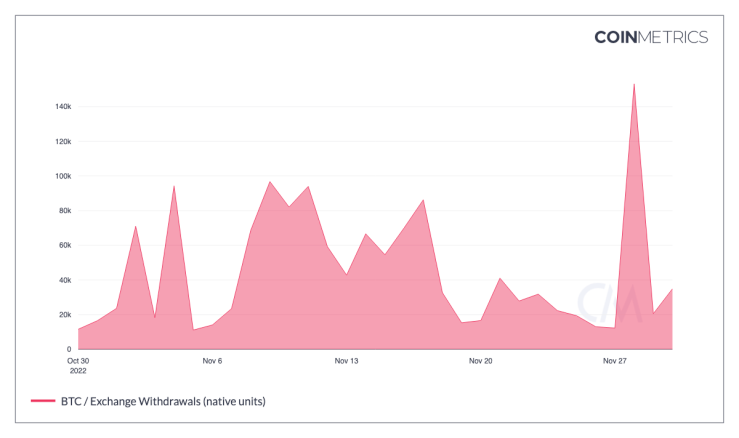

In reaction to the FTX fraud, most remaining BTC holders have decided to “become their own banks.” That means they’re moving their assets into cold storage, such as offline hardware wallets, for safekeeping, rather than trusting black boxes with their funds.

Viewing the chart below, we can see this migration taking place. Since the start of November, over 220,000 BTC (~$3.7 billion USD value) has been transferred from exchanges into cold storage.

While the FTX fallout has accelerated this exodus, the total amount of BTC left on exchanges has been dropping daily since October.

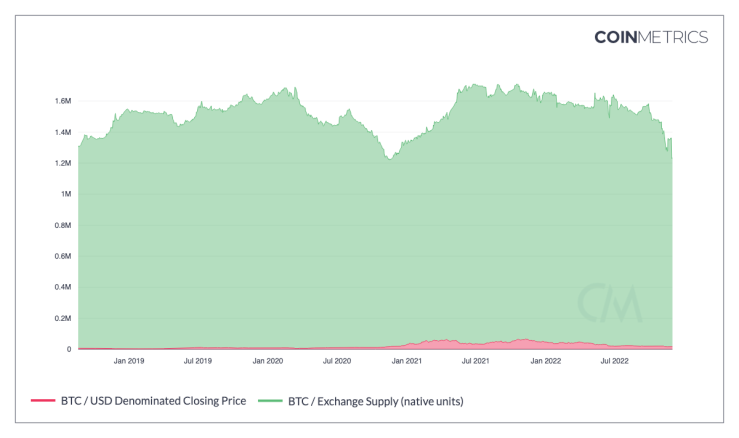

As a result, exchanges only hold about 1.2 million BTC total at present. That’s the lowest amount since November 2020, just before BTC broke out above $20,000 and started the parabolic phase of its bull run.

Coins leaving exchanges has three primary effects on the market:

- It will help us to quickly identify which other exchanges are insolvent. As the old adage goes, “only when the tide recedes will we see who’s been swimming naked.”

- This activity brings Bitcoin back to its roots as a bearer asset and USD alternative (more on this next week - be sure you're subscribed).

- It makes the market illiquid and thus more prone to large price movements.

If the worst of the FTX saga is now behind us, this lack of spot liquidity could become a magnet to the upside into the end of 2022. But that’s a big if.

In “Welcome to the Jungle,” we discussed liquidity pools and showed high value target areas with large amounts of open interest. Below we see them updated, and though the upside remains ripe for the squeezing, there is now a large long liquidation pool in the $14,000 range which is becoming more vulnerable of being tagged by the day.

Not included in these liquidity pools, however, is the world’s largest purveyors of “paper” Bitcoin, and biggest squeeze target of all: institutional bear whales on the Chicago Mercantile Exchange (CME).

Allow me to explain…

Hunters Becoming the Hunted?

The CME is home to some of the most sophisticated and experienced institutional traders on Earth.

As discussed last week, regulations in the U.S. do not allow for spot Bitcoin holdings to be margined. U.S. traders seeking leverage can only trade Bitcoin futures contracts that are margined and settled in dollars on the CME.

This means that when U.S.-based institutional money wants directional exposure to Bitcoin’s price, the CME is where they go.

In simple terms, trading BTC futures at the CME is a lot like going to your local bookie and making a bet in cash that on X date, the price of Bitcoin will be higher or lower than X price.

Regardless of who wins or loses the bet, neither party is required to ever actually buy or sell Bitcoin. They only owe the other person cash. This is in contrast to almost every other asset in the world where you must own or borrow the underlying asset in order to short sell it.

At times of heightened fear and uncertainty, these cash-settled contracts create a one-way market. One where there are far more sellers than there would be in a natural, spot-settled market that would require exposure to the underlying asset.

When this happens, the price of futures contracts falls below the price of BTC itself. This phenomenon is what is known as “backwardation,” and we see a current example of it below.

On this chart, notice how the spot price of BTC on Coinbase (blue line) had been trading consistently higher than the CME’s March 2023 BTC futures (orange) contract in recent months.

This means that if you wanted to short March BTC futures on the CME October-December, you had to pay a premium to do so and start your trade at a loss.

Such irrational behavior is usually the byproduct of what’s known as “ambulance chasing,” a term used to describe speculators looking to profit off a dying company or asset by crowding into short positions. Extreme greed to the downside.

Such appeared to be the case with CME traders in the wake of collapse of FTX.

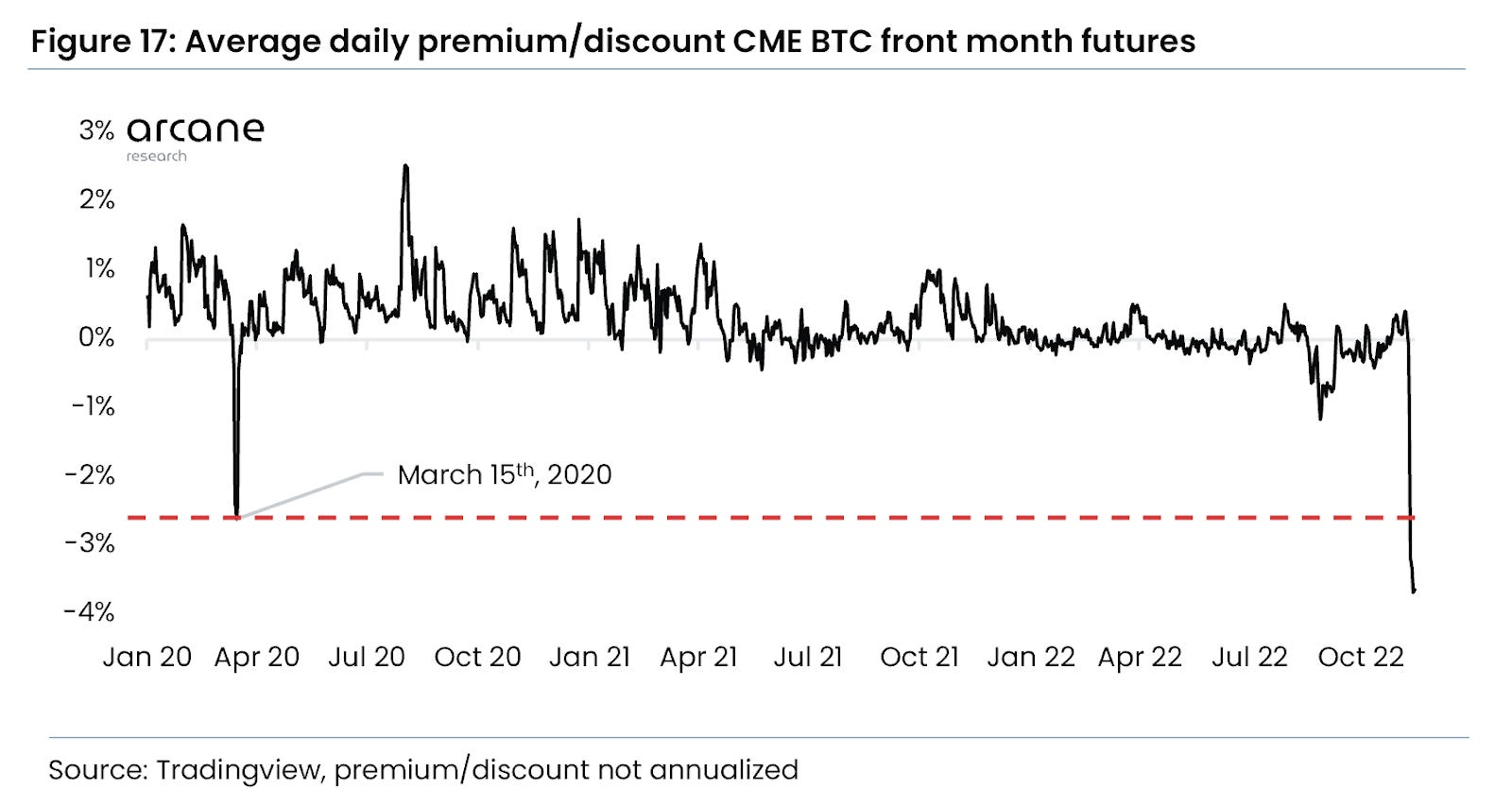

Below, we see the average daily discount of BTC on the CME reach the lowest it’s ever been last month, even lower than in March 2020, when the COVID crash nearly sent Bitcoin to zero.

Through the data, we can see just how anxious these ambulance chasers were to cash in on what they presumed to be the death of Bitcoin.

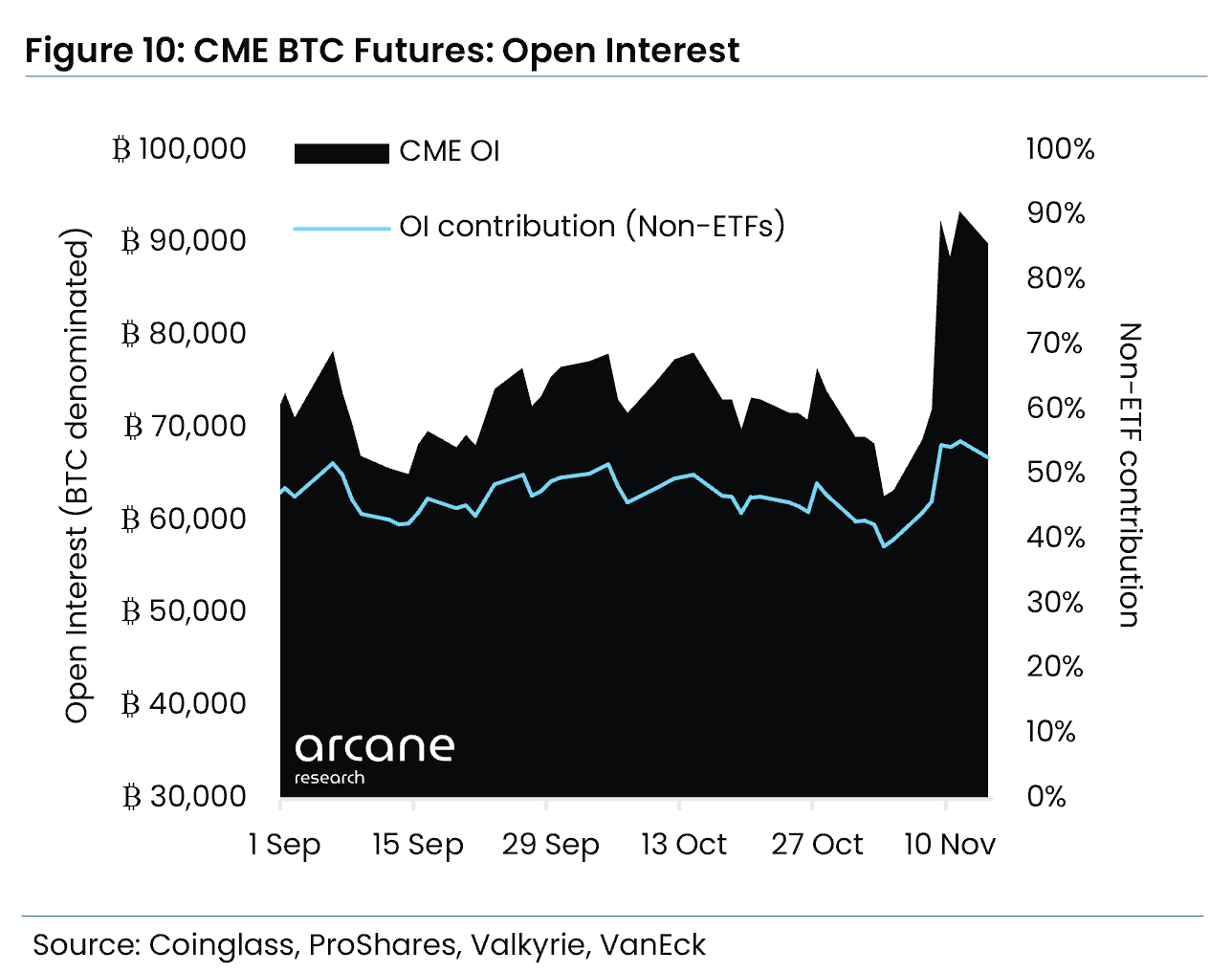

Following FTX’s bankruptcy announcement during the week of November 7th, about 30,000 BTC (~$510 million) worth of additional open interest rushed in to short BTC on the CME.

That means between FTX and CME alone, over 100,000 BTC (about $1.7 billion) was sold in a matter of days, and yet the price remained resilient.

That’s an encouraging sign as such one-sided sentiment in any market not making new lows is typically signals a move reaching exhaustion.

Think for instance about some of the absurd premiums we saw on futures funding rates in 2021, and how quickly the market would crash, correct, and clear the inflated open interest.

This is that same dynamic in play to the downside.

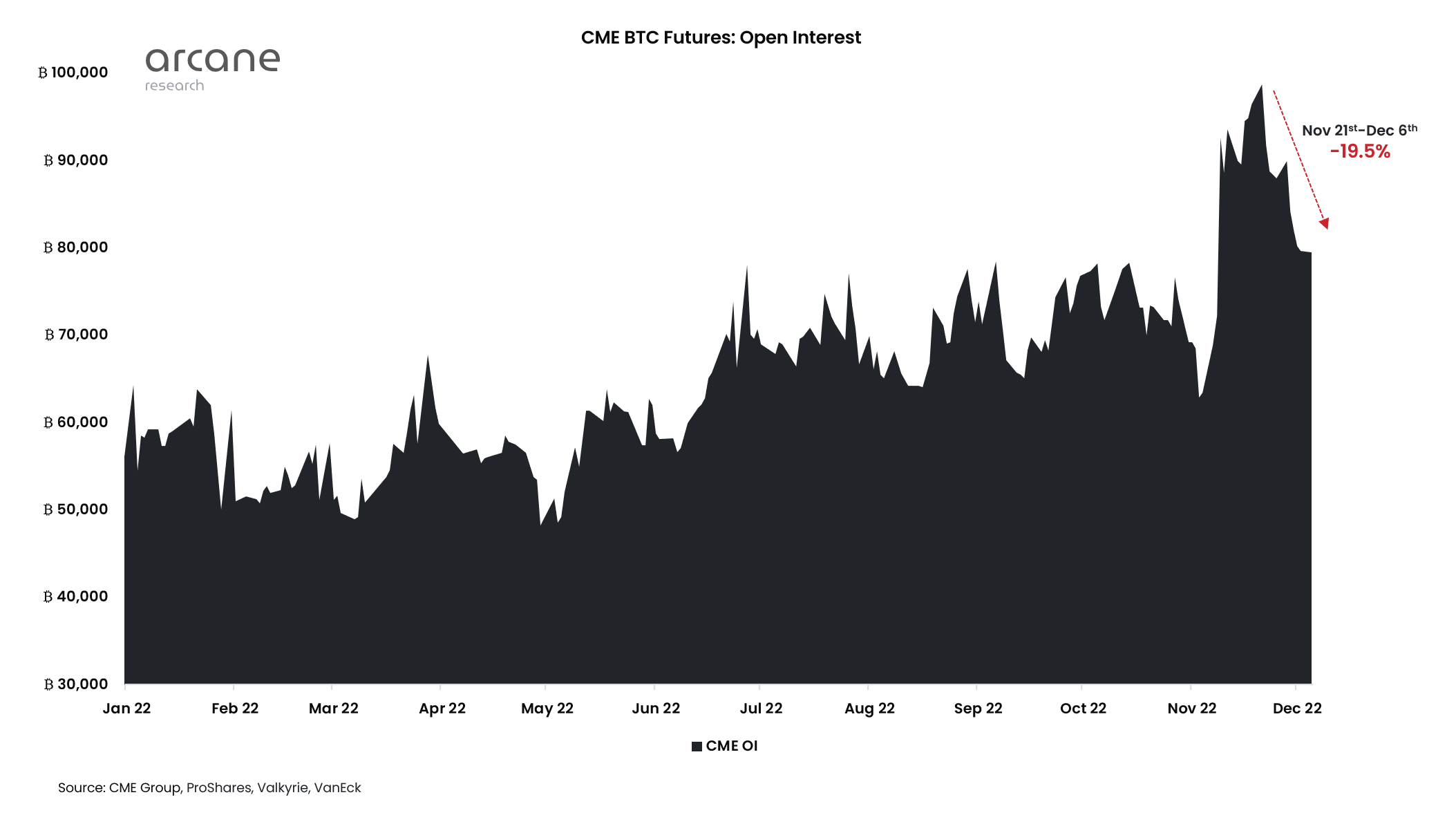

In recent weeks, it seems some CME players have recognized this danger and closed out their shorts, as CME open interest has now dropped nearly 20% from its November high.

The paper shorts still remaining are speculating heavily on another wave of contagion striking BTC and decimating its price.

However, judging by how late many of them were to the short side of this trade, it is also likely that those still remaining are “headline traders” who aren’t native to this market. Because of this, it is unlikely most are aware of the lack of spot liquidity we discussed above, and the extreme tail risk it presents for them.

Should the market find its footing, it won’t be long before savvy market participants figure out how to profit off of squeezing these remaining shorts. The bounty is just too big to ignore. Couple that with the increased likelihood of volatility due to spot supply leaving exchanges, and things could get quite interesting soon.

For every action, there is an equal and opposite reaction, and the last place you want to be as a seller of paper Bitcoin is on the wrong side of a spot-driven rally.

Such a move could result in these CME ambulance chasers, rather than Bitcoin, being the ones in need of emergency rescue…

What do you guys think?

Leave a comment below or message me on Twitter @JLabsJanitor.

Likes, shares, and subscriptions are always much appreciated as well!

Your friend,

JJ