Tempering Expectations

The Blend: Looking Back on Arkham's Drop; The Stock-to-Flow Model’s Strength Isn’t Predicting Price; FedNow Embracing Web3?

When I’m really bored, I run.

Doesn’t matter the time, the day, how hot or cold it is…

I just step outside and go. Half the time I don’t care what I’m wearing either.

And to really just let the boredom take over, I might even start chanting…

“Hum nah nah nah nah nah nah nah Hum nah nah nah nah nah nah nah”. That’s quite literally what it sounds like.

Not sure what it is, but this rhythmic humming almost forces me into a trance. I got so lost in boredom during the pandemic one night while throwing a few back that I ran for nearly two hours in darkness.

Talk about a good time…

Anyways, I’m reminded of those days as this crab market continues.

But instead of running, our team keeps showing up each day, trying to improve a little bit at a time.

The same goes for you on the other end… You also continue to show up and prepare.

Both of us stuck in our own versions of a chant…

Repeating to ourselves that hard work pays off. It’s a mantra we know if we get lost in and persevere through, the reward will come.

To those that embrace these dull periods and become more Spartan like, I raise my cup to you.

And then continue to run…

With that, let’s get to today’s blend of pieces that remind us to not get overly hyped at the slightest signs of good news. Temper expectations and we’ll find the gems ahead.

PlanB Neglects Your Appetite For Small Caps

Look who’s back.

PlanB, the independent analyst who made Bitcoin’s stock-to-flow (S2F) model so popular, is making wild predictions once again.

For the uninitiated, stock-to-flow is a figure that is a ratio of the market cap of a commodity (e.g., gold, silver, and even Bitcoin) to the amount of new supply of the commodity created in a year.

PlanB famously plotted this ratio for Bitcoin’s existence and used it as the basis to model future prices of Bitcoin.

Now, PlanB has received a ton of hate over his model, and to be fair, much of it is for good reason.

He used it to put out wildly massive claims on the future market cap of Bitcoin. Then when he was wrong, he seemed to just brush it off by basically saying, the models are just that, models.

And he most recently gave a price prediction between $100,000–$1 million, which is the equivalent of the broad side of the barn in terms of targets. Hate deserved.

But I’ll be the first to admit: I sort of like the model. It has some merit.

It does show the relationship between an asset’s supply and its market cap: Increase the new supply coming into the market, reduce the price of the individual asset.

But while S2F is very good at modeling this dynamic, that also alludes to one of its flaws.

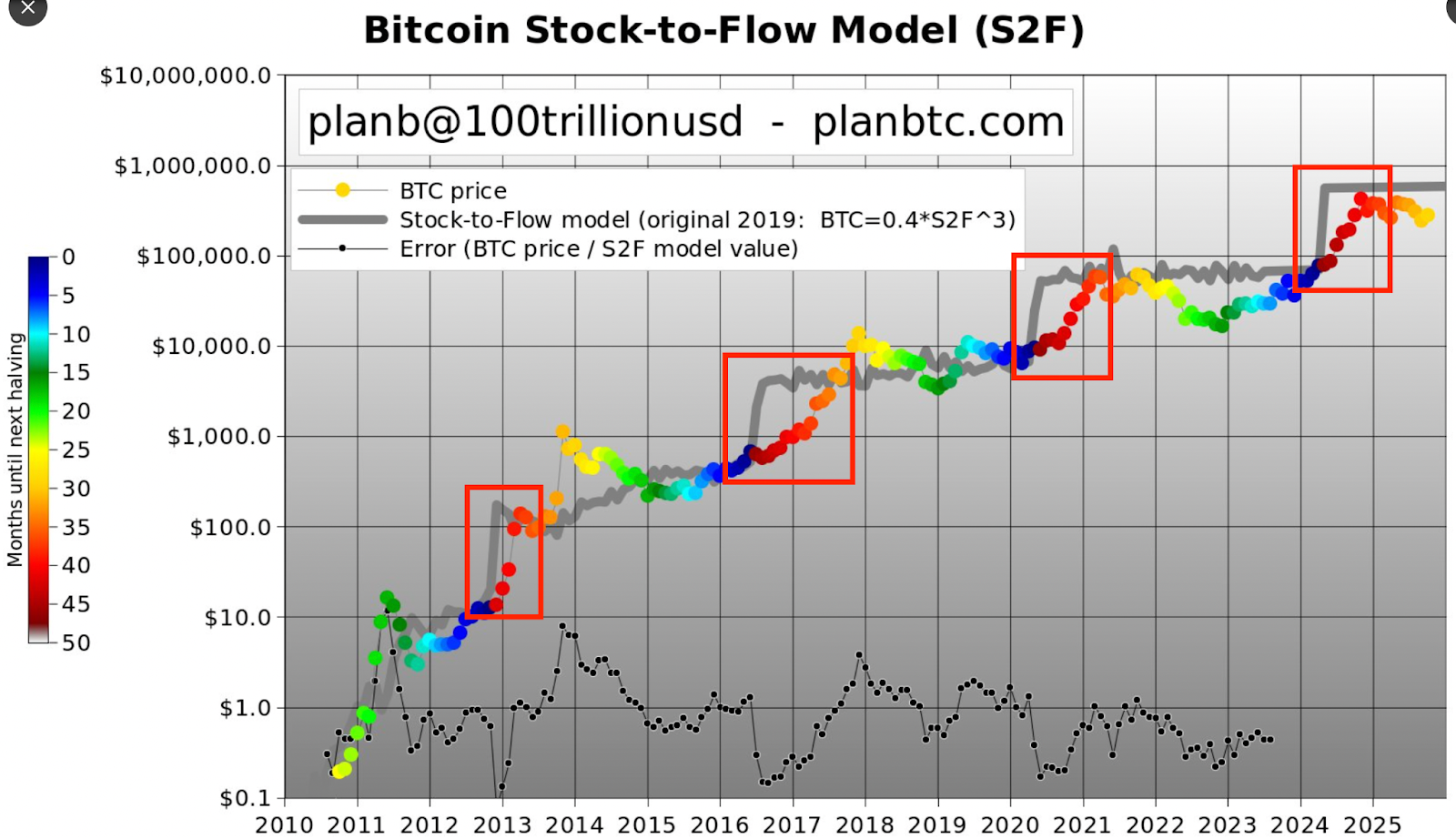

Here is one of PlanB’s most recent price prediction charts. It looks a bit odd because he plotted some future dots on the chart. It’s how he came up with his recent target of $500,000 or whatever it was.

The gray line in the chart represents the model’s predictions for Bitcoin’s price, and the line of colored dots shows its actual price change over time. The color of each dot represents how many months away the next Bitcoin halving is, from zero months (dark blue) to more than 40 months (dark red). (Don’t worry about the third line of black dots closer to the bottom.)

What I’d like us to focus on is the red boxes. Notice how the gray prediction line jumps with a halving. But the colored line showing price actually responding takes a little longer to climb higher. There’s a lag effect.

What we see is price takes time to respond to this change in supply flow. And S2F is a really great illustration of this idea in practice.

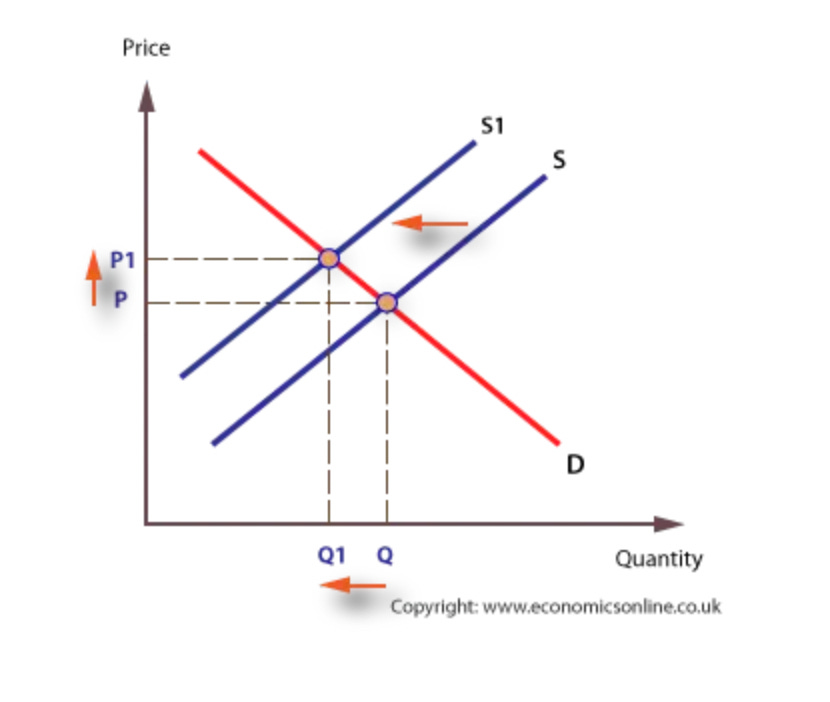

In the chart below that might remind you of Econ 101, Bitcoin’s halving moment is the shift of the supply curve labeled “S” to “S1”. It’s a supply shock. Without a change to demand, the market finds a new equilibrium price that’s higher.

(This chart doesn’t perfectly represent Bitcoin’s supply curve, which is more straight up and down while its demand curve is more horizontal. I’m just using it to illustrate the broader concept.)

Anyways, getting back to why this is relevant to the S2F model… In the chart above, there’s a red line labeled “D.”

S2F does nothing to address this line of demand. And it’s the glaring flaw in the model and why it will never be fully accurate.

That’s because in the boring world of economics, we look at both supply and demand. And just because supply changes, doesn’t mean demand sits still.

In fact, what is bound to happen is when price starts to rise, the consumer begins to look at substitutes. For Bitcoin maximalists and Michael Saylor, there is no second best. There’s just Bitcoin.

But in reality, the market is much larger than those two demographics. How many of you own more than just Bitcoin?

Better yet…

How many of you are likely to prefer a token with a lower market cap over Bitcoin once a bull market arrives? I imagine quite a few of you. This market response is why the demand curve begins to shift once supply shifts.

The market is not linear, and it’s not isolated. When you look at PlanB’s models in the future, I don’t want you to necessarily discredit them. Just realize what their shortcomings are. And apply this reasoning to it.

They don’t take everything into consideration. And they’re really not meant to. Which is what PlanB is likely alluding to when he says it’s just a model – a model of supply’s effect on price. But that’s only half the equation.

What it does a good job, though, is remind us of a simple fact… These supply shocks cause the market to find a new equilibrium with a lag effect. So while I agree we shouldn’t overly hype the S2F model, we also shouldn’t be too quick to discard it.

After all, just go back and look where the light blue dot sits relative to these cycles… Pretty low, right? It’s a pretty nice dose of modeled hopium that has some merit.

FedNow Dropps A Bombshell

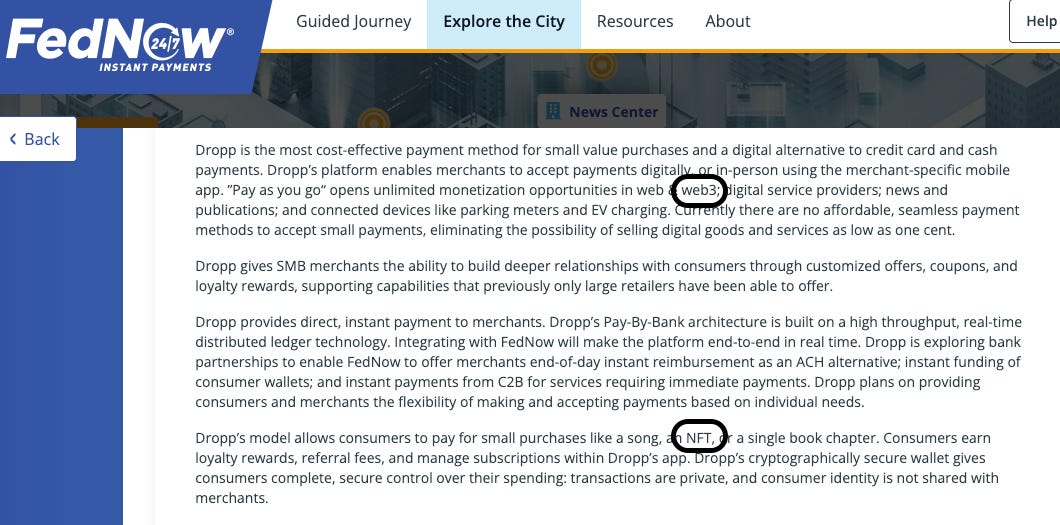

If you go on the FedNow website, you can now find the words Web3 and NFT in black and white.

Don’t believe me? Here’s a screenshot that you can tape into history books.

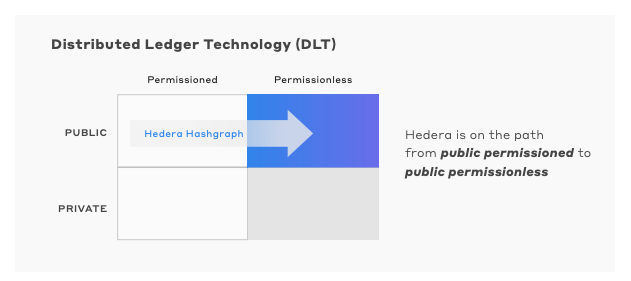

The text in the screen grab above describes a payment solution called Dropp. It uses a “decentralized ledger technology” (DLT) that facilitates micropayments. That DLT is Hedera Hashgraph.

As you can imagine, the Hedera community is going ballistic (its token, HBAR, was up as much as 20% this week). And for good reason. After all, one of the apps on its chain is now listed on the future payment system being rolled out by the U.S. Federal Reserve. It’s likely to be one of the major pieces of tech on the largest settlement system in the world. That’s massive.

But if we look deeper into the news, we start to tap the brakes.

That’s because Dropp is one of 108 projects listed on the site’s showcase… meaning FedNow is giving examples of how to include the technology into a business. But it doesn’t necessarily mean anyone is using it.

Now, to be fair, it appears Dropp does have every intention to bring FedNow into its application as it’s listed in its roadmap. And it did do all the work required to get noticed by FedNow, so it must have something behind the curtain on that front.

Yet, I go back to the main question: Will it actually happen? Only time will tell. But one thing that made me take note was the fact the website makes sure to include this caveat on every single page:

The materials made available through this showcase are presented as a convenience to potential participants in the FedNow Service. Federal Reserve Financial Services (FRFS) is merely the host for the showcase and does not support or endorse any showcase providers.

So Dropp’s presence on the site is not an official seal of approval. But it’s something. And that something is permissionless, decentralized, and open source… Right?

If you’re not familiar with Hedera, it’s not a permissionless network. Its nodes are operated by a council that includes Fortune 500 names. A quick glance at the list reveals Google, IBM, Boeing, LG, T Mobile, Dell, and others listed as your gatekeepers.

That doesn’t feel very Web3. At least it’s not the way I envisioned Web3 to look.

But in all reality, how decentralized are layer-one networks outside of the majors like Ethereum and Bitcoin? I can’t imagine they are any more decentralized than what we see with Hedera.

Granted, I’d prefer not to see some of those Web2 titans listed as the validator to my transaction. But is not knowing who the validator is any better? Not sure I’d agree with that.

And to be even more fair, Hedera does lay this out in the open. It’s published a plan to become permissionless.

So here I am, wavering back and forth on whether this will happen and if it’s truly a step forward for Web3.

What I’m settling in on is that Hedera at least is open about its desire to be permissionless. That should count for something. It beats what we might see coming out of JPMorgan and its permissioned network, where more than 400 of its own banks sit. I would fully expect them to tout decentralization, even though they all march to Dimon’s orders.

But when it comes to FedNow, what does this mean?

I’d argue it’s a good thing. It’s a step in the right direction. My belief is that fully decentralized, permissionless, and open-source solutions will not be allowed at first. There’s still a desire for more composability, verifiability, and transparency. Which might mean less ideal solutions will need to be adopted and broken, first.

And honestly, I expect some of the advancements toward this decentralized and permissionless future to happen with a “beg for forgiveness” versus “ask for permission” approach.

What I mean by this is somebody will find a way to custody FedNow digital dollars and tokenize them on Ethereum or another blockchain. The Federal Reserve won’t like it, Senator Warren will cry, Sherman might talk about Mongoose Coin again, and advocates for self-sovereignty and privacy will go ahead and fight.

It’s the unfortunate reality of how crypto keeps pushing that Overton window to a more transparent future.

In the meantime, while we wait for a developer to pounce on one of those opportunities, it’s great to see FedNow host the words “Web3” and “NFT” on its website. Even if it’s just for show. We have to start somewhere.

And as far as Dropp, all we can do is observe. I fully expect to see KYC/AML happening on the app, which means the ability to monitor users will be very high. It also means the crypto-native users Dropp might try to attract will pause in their tracks as they go through the onboarding process.

I also don’t see Dropp competing with other services listed on that site, like Plaid, which has 200 million accounts with 11,000 bank connections to date.

It was news that made a splash, but don’t expect too much follow-up here.

The Arkham Token’s Utility In One Picture

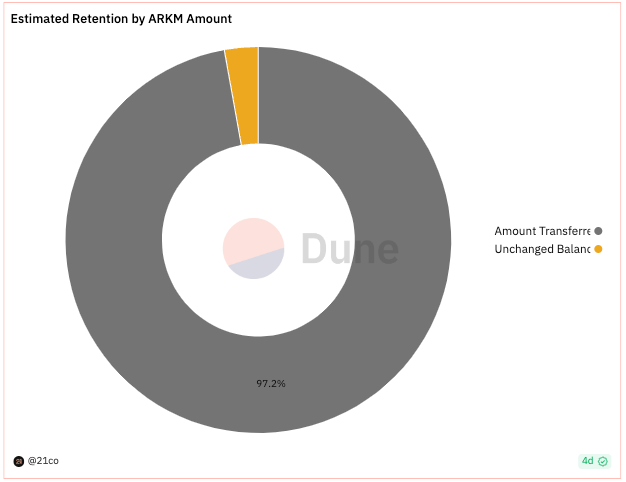

97.08% of Arkham’s native token (ARKM) was claimed during the airdrop that took place a month ago to users of the Arkham platform.

That’s impressive.

Now, the reason the blockchain explorer needs a token is for what many have called the snitch-to-earn exchange, or Arkham Intel Exchange.

The exchange allows users to submit bounties to find certain addresses or the identity behind certain wallet addresses. Part of this process requires users to lock up tokens as proof of payment.

Once an individual submits proof of intelligence – the information requested – then Arkham reviews the information. If accepted, then the settlement procedure unfolds.

Now, to see how successful the exchange was, I went ahead and looked at the recent listings. There were 22 in total. The amount of ARKM at stake here was 181,000 tokens.

82% of all these tokens were tied up in two listings, meaning most of them were not worth much considering the token is trading at $0.40 as I write.

What this tells me is that demand for wallet labels is not very high. If it were, we would see a lot more bounties.

Second, the exchange is vulnerable. Arkham is sitting there verifying whether something is worthy of pay. And it doesn’t have much volume. That’s a recipe to force a round peg in a square hole.

And what are the consequences here if somebody requests a bounty on a hacker, somebody submits decent docs that are falsified, and Arkham approves it hoping to drum up interest in its exchange? The damage to social reputation is pretty stiff.

And where do you even push back against a claim, which is sure to cost a pretty penny considering how Arkham was doling out lawsuits for anybody that badmouthed it?

Opinion on social media is one thing. Going through a bounty process like this is another.

The fact is the system seems vulnerable. And the token is not really achieving what a cryptocurrency should be achieving… Which is to reward those that secure or put forth the value of the system. Last I checked, the emissions are not going to those who are labeling wallets or securing bounties.

This translates to the token having a massive disconnect between its intrinsic value and the function of the protocol.

Which is in part why we see this type of chart. Nearly all that claimed the airdrop have already moved the token out of their wallet.

What’s more…

Over 64,000 wallets claimed ARKM, but now Etherscan shows just over 16,000 holders. Perhaps most are sitting on exchanges?

To check, I went and looked at Arkham’s dashboard. It shows Binance received 100 million ARKM deposits over the last 30 days. Meanwhile, only 30 million were allocated to the drop.

Not sure what the net is, but I have to imagine it’s more than 30 million and likely this number is bigger due to market makers having a percentage.

To further showcase how this token is viewed in the market, we can see that nearly all the tokens are either on exchanges, held by Arkham or one of its employees, or locked in vesting contracts.

And while the first major unlock is not until a year after the drop, this is rather concerning. The majority of the supply looks to be in the hands of those that need capital (Arkham) and speculators. Not users.

Which is to say that the token has low demand for the reason it was created.

For now, the token’s main use case looks to be speculation. And since the largest entities holding liquid tokens outside of exchanges and Arkham are market makers, I wouldn’t be surprised if this token has some strong price action in the weeks or months to come.

But don’t be fooled. Any price action to the upside with news that does little to drive demand for the token is sure to be short-lived.

For full disclosure, this piece is purely just my opinion. Do your own due diligence to come to your own conclusion. Read Arkham’s whitepaper and check the chain for hard data.

As for now, it looks like the airdrop was yet another cash grab with little follow-up. I would hope to see things change with Arkham and its token, but I don’t feel optimistic.

After all, Arkham’s main Twitter account is tweeting 40% less over the last 30 days. Maybe when it picks back up that’ll be your sign.

Until next time…

Your Pulse on Crypto,

Ben Lilly