Alonso and Sancho

Macro Update: The UK and EU are Straining

Famous duos.

There are plenty of them, both fictional or real.

Adam and Eve. Laurel and Hardy. Hans and Gretel. Sonny and Cher. Butch Cassidy and the Sundance Kid. Garfield and Odie. John and Yoko. Just to name a few.

One pair you likely hadn’t heard of is Alonso and Sancho.

If we use Alonso’s other alias, then people will start nodding their heads. Alonso is also known as Don Quixote, the main protagonist in one of Spain’s most renowned literary works, The Ingenious Gentleman Don Quixote of La Mancha, written by Miguel de Cervantes in 1605.

The picture above is the actual house that author Cervantes stayed in while he was in Cordoba, Spain.

The picture below is a magnified white plaque on the wall that commemorates and marks the house as a special designation.

The majority of people have heard of Don Quixote. However, his sidekick Sancho, a farmer whom Alonso (Don Quixote) recruited as a squire, is hardly ever mentioned or recognized.

While I travel through the country I find myself thinking of the similarity of this duo with the United Kingdom (UK) and the European Union (EU).

To better explain, let’s break down UK today, and then focus on the EU in the next update.

Truss Me

Liz Truss was installed as the new Prime Minister (PM) of the United Kingdom after Boris Johnson resigned on September 6, 2022.

She is taking over the office in the midst of the highest inflation that Britain has seen in three decades.

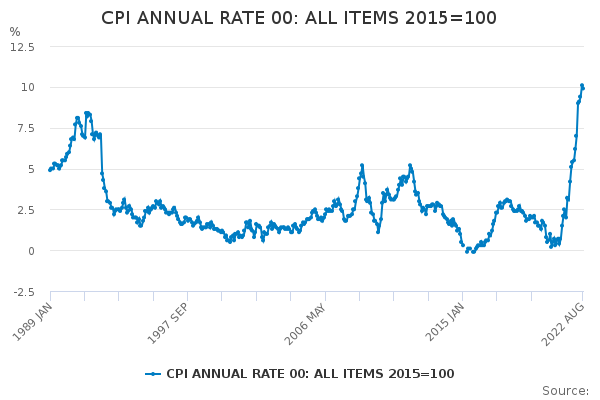

Source: UK Office for Online Statistics

The UK consumer price index (CPI) hit a high of 10.1% in July 2022 and the August CPI sits at 9.9%. As you can see in the chart above, this is the highest its been in over 30 years.

The other part is the United Kingdom has been battling with this inflationary pressure since the day it voted for Brexit.

The Brexit vote started out as a “I dare you” referendum by the then over-confident PM David Cameron. Cameron felt so confident that the referendum would not pass and since he is the man of the people, he allowed the referendum to be on the ballot and the rest is history.

A consequence of the UK exit from the EU is that the UK no longer has access to cheaper produce, food, and other goods from the EU region.

Also, the Schengen Agreement of the EU no longer applies to the UK. Hence EU member citizens are not able to move in and work freely in the UK like they did once before.

We are now beginning to see the effects of this decision.

In fact, this is putting a huge strain on the UK’s labor market. A large portion of the UK work force were from the Eastern European countries prior to Brexit. Now this pool of cheap labor is no longer available to the UK.

To make matters worse, toss in soaring energy costs. And as we see the Bank of England has no choice but to combat this inflation by aggressively hiking interest rates.

This started at the end of 2021. The interest rate has gone from 0.10% back in November 2021 to 2.25% today. You can see the rate at which this is rising in the chart below.

As a result of this hiking, the yield for government bonds from the United Kingdom, also known as Gilts, began to climb just as fast.

Below, we have a chart of the yield on the 30-year Gilt. Please note the green box in the chart below, this marks the start of 2022 when Gilts began to surge higher.

The yield on the 30Y Gilt has been surging since the beginning of 2022 - right when rates began their climb.

As for the red box, we will circle back to that parabolic move shortly.

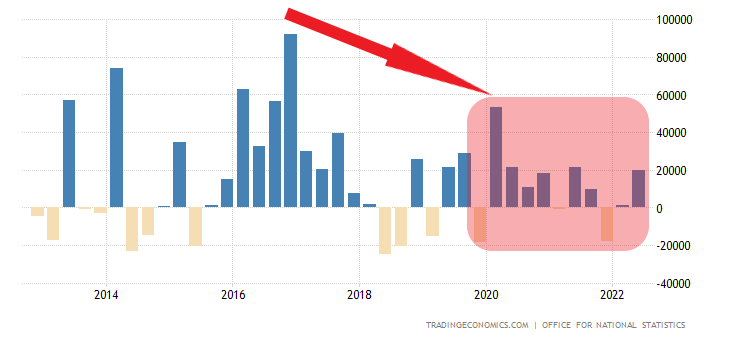

But first, I want to bring up another reason for why the recent issues are unfolding in the UK. Its the decline in foreign direct investment (FDI). Foreigners are not as interested in what the UK is selling.

The chart below shows FDI, and it has been gradually declining for the UK since 2017. The red box below shows FDI since the Brexit decision in 2020.

Thanks to Brexit, UK goods can’t enter the EU market without tariffs. Combined with the restricted terms of trading with the EU, the UK fails to convince foreign entities to invest in the UK.

It goes without saying that Truss inherited quite a hot and sticky mess.

With potential runaway inflation, trouble in the Gilt market, and declining economy, Truss decided to take action.

Her decision was to mimic the strategy of a former U.S. president who helped get his country out of a similar quagmire.

Reaganomics, UK Style

To say that Liz Truss is a fan of the free market is an understatement.

As a Conservative Party Member of Parliament (MP) back in 2010, she and four other MPs (most notably Kwasi Kwarteng, who is the Chancellor in Truss’s cabinet) from the same party co-authored a book called Britannica Unchained: Global Lesson for Growth and Prosperity. The book adores free markets, less government intervention, and fewer regulations for the economy to prosper.

With similar economic headwinds like the U.S. back in the early 1980s, Truss is trying to simultaneously curb inflation while sparking the economy. So she decided to follow the playbook of Ronald Reagan: She’ll let the BoE hike interest rates to battle inflation, and at the same time, she’ll roll out a new tax-cut plan in hope to stimulate consumer spending. Which is what Reagan did back in 1980.

Unfortunately, Truss’s tax cut plan sent shockwaves through the financial system in the UK.

The announcement and the details of the tax cut came right after Truss announced the UK energy subsidy plan. The UK will subsidize every household for the upcoming winter and the plan will cost approximately 150 billion British Pounds (GBP).

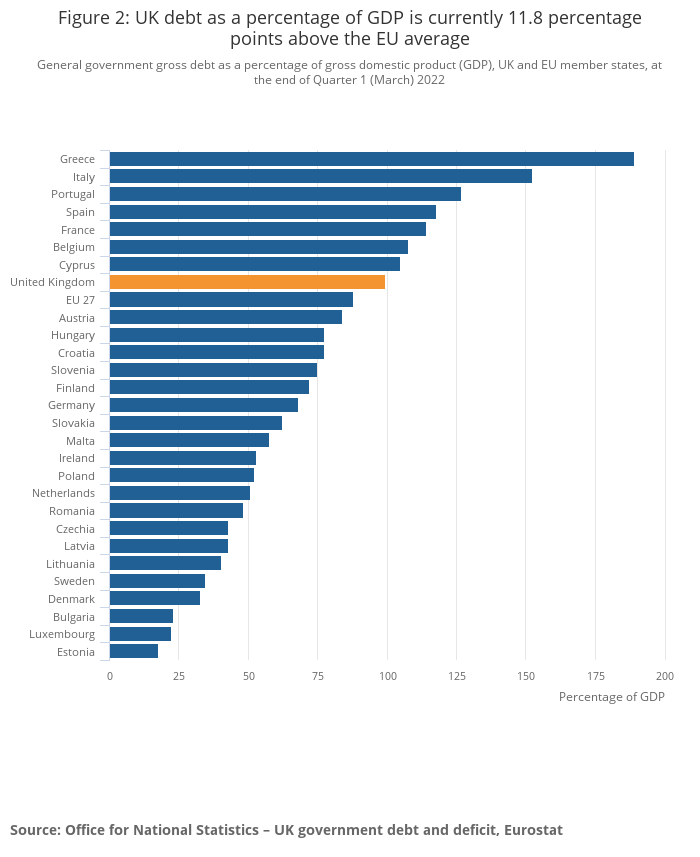

One likely reason for such a shockwave is that the UK also has one of the highest debt-to-GDP ratios in Europe. We can see this in the chart below.

Source: UK Office for Online Statistics

No one in the world believes the UK can afford to roll out this tax cut plan.

The response - investors started to sell Gilts, fearing the UK government would default. This sent the 30Y Gilt yield much higher.

Time to bring back the red box from earlier, I dropped the chart below so you don’t need to scroll back up.

The red box is the parabolic surge in the 30Y Gilt yield that came right after Truss’s tax plan announcement.

The selloff of the Gilts translates that this liquidity is looking for a place to go. With a strong USD and a hawkish U.S. Federal Reserve, investors are switching to U.S. assets. The U.S. dollar index (DXY) is up over 17% on the year.

This flee away from the UK resulted in a massive British Pound selloff. And therefore, the exchange rate between US Dollar and British Pound (GBPUSD) almost went to parity or 1:1. That is shown in the chart below.

To make matters even worse, the Truss government stepped in and started buying the Gilts.

The government is buying its own debt. Reason being, it needed to prevent the yields from surging due to pension funds.

Enter the newest derivative to go from obscurity to popularity thanks to a major selloff - LDIs.

The fund managers for the UK’s pension funds have met with margin calls to post more collateral from the strategy they adopted by using a derivative product called Liability-Driven Investment (LDI).

To put it in simple terms, LDI’s concept is to allow the fund managers to get exposure to long-dated financial instruments so the pension funds can meet long-term cash flow needs.

As of 2020, the LDI amount boomed to 1.5 trillion GBP.

When the yield of the underlying asset (in this case, the Gilt) for the derivative product such as LDI is low, then the fund managers are above the margin. But when the yield skyrockets like what the Gilt just did in the past few weeks, then fund managers will get margin calls and they will need to put up more collaterals/cash to maintain the margin balance or they risk liquidation.

The fund managers start to sell the Gilts they have to raise funds and to post more collateral to avoid liquidation. The Gilts keep getting sold off. The yield keeps ticking higher. The fund managers are met with another round of margin call as the yield spikes.

It is a vicious cycle. And this is why Gilts were plastered on headlines recently.

It meant the Bank of England had no choice but to intervene and start purchasing Gilts in order to rescue the UK's pension fund. It was on the brink of collapsing.

It’s been pins and needles since then.

And to really make the market more anxious, Andrew Bailey, the governor of the Bank of England, distinctly announced on October 11, 2022 that the BoE will allow the fund managers only three more days to unwind any trading positions that are not sustainable. On Friday, October 14, 2022 - today - the BoE will stop buying Gilts and leave the market dynamic to work itself out.

Is Bailey bluffing? Will the market call Bailey’s bluff?

We will find out soon. And as we roll into Friday we will start to see what’s next.

The First of its Kind

Bringing this back to the tax cut discussion earlier, the 45 billion GBP or $48 billion dollar tax cut that started this entire financial disruption was scrapped.

If Bailey retracts and continues to buy Gilts after the ultimatum, the UK might be the first in the world to do market tightening via interest hikes and run a market easing campaign by printing money to buy its own bond. Tightening and QE.

This is truly unchartered territory.

And if Don Quixote inspires us to take action, the UK is filling the role.

As far as the masses that represents Alonso, we will focus on the European Union in the next macro update.

Until things calm down and find solid footing in stocks and crypto especially, it is important we are aware of global situations such as this.

Thank you for reading. Much appreciated.

Yours truly,

TD